This challenge can often be a simple supply-demand contradiction: to build more housing (and thus reduce rents), we need more construction workers. But those additional workers need places to live themselves while they're building the new homes. This creates a temporary increase in rental demand—potentially driving up the very rents we're trying to reduce. It's a cycle that makes housing markets particularly difficult to stabilise quickly.

Four key factors drive rental growth, each with its own complexities.

Investment in rental housing significantly affects supply. When interest rates rise or property investor confidence falls, fewer rental properties enter the market. Investors may choose to put their money elsewhere, leading to stagnant or shrinking rental stock. This creates fierce competition among tenants for limited housing options, pushing rents upward. During periods of low rental investment, even modest increases in demand can trigger substantial rental growth.

Population growth, especially through migration, creates immediate demand for housing. Unlike gradual natural population increase, migration can rapidly change local housing needs. International students, skilled workers, and interstate movers all require accommodation almost immediately upon arrival. This sudden demand surge often hits markets before supply has any chance to adjust, creating pressure points in rental markets that can take years to resolve.

Rising wealth and income levels amplify rental pressures in unique ways. As household finances improve, people can afford to spend more on housing—either upgrading to better rentals or bidding more aggressively for desirable properties. This economic capacity doesn't just affect high-end markets; it creates ripple effects throughout the entire rental market as competition increases across all price points. Even modest income growth across a population can translate to significant rental increases in desirable areas.

Perhaps most overlooked is the impact of changing household composition. When people "spread out" into smaller households—whether due to lifestyle preferences, ageing populations, or relationship changes—the same population suddenly needs more dwellings. During COVID, Australia experienced exactly this, with average household sizes shrinking. This dramatically increased effective housing demand without any actual population growth, putting unexpected pressure on rental markets nationwide.

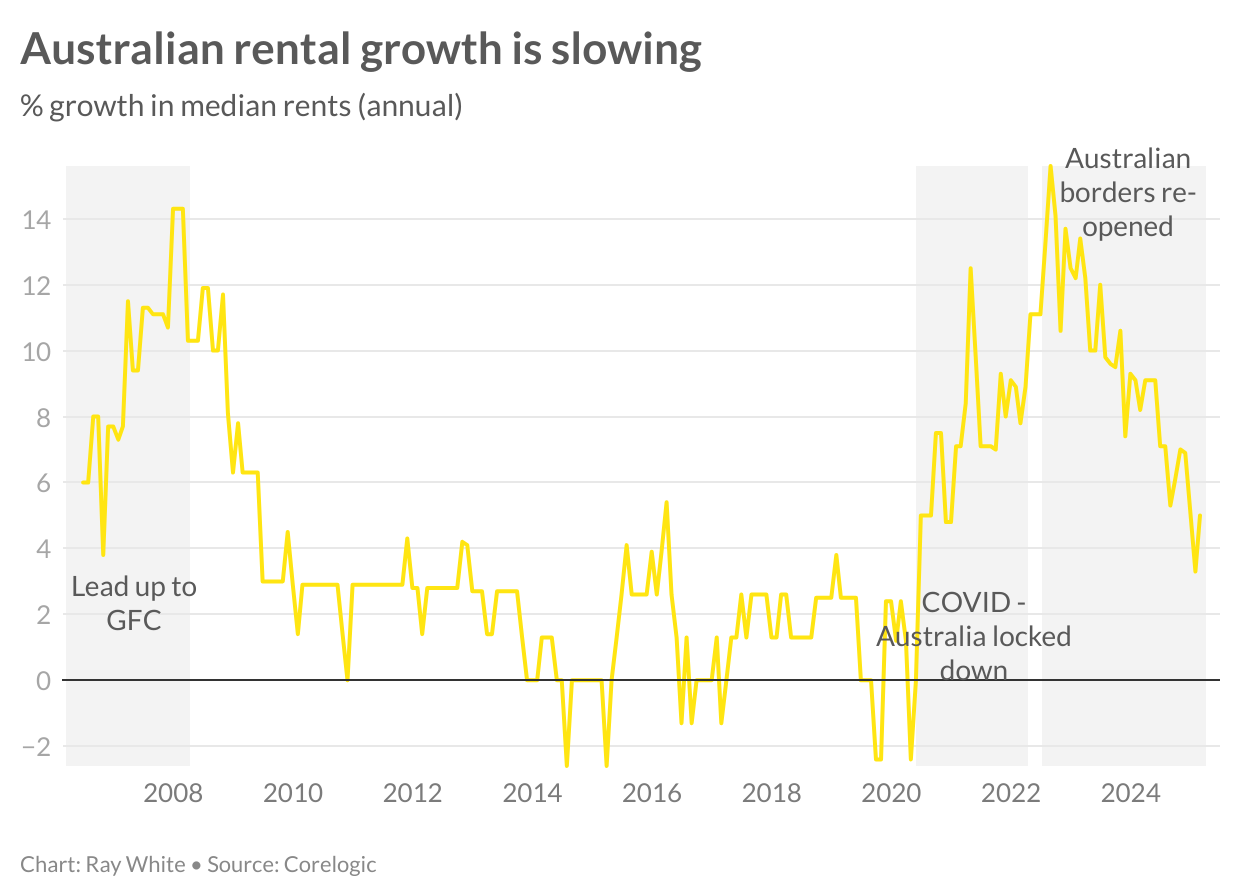

Australia's rental market has experienced three significant surges over the past two decades. The first came in the lead-up to the Global Financial Crisis (GFC), fuelled by strong population growth and rising interest rates that discouraged investment in rental properties. The second occurred during the COVID-19 pandemic when, despite negative migration, increased savings and changing living preferences led many Australians to seek more space—creating a sharp rise in single-person households and reducing average household size. The third surge happened as international borders reopened post-COVID, when the spread-out population collided with limited rental capacity and an influx of arrivals.

Now, we're seeing a national slowdown in rental growth. Average household sizes are returning to pre-COVID levels, creating additional capacity in the market. While housing supply remains challenging, more homes are being built, and migration has stabilised. The national data shows rental growth declining from peaks of over 15% after borders reopened to around 5% currently.

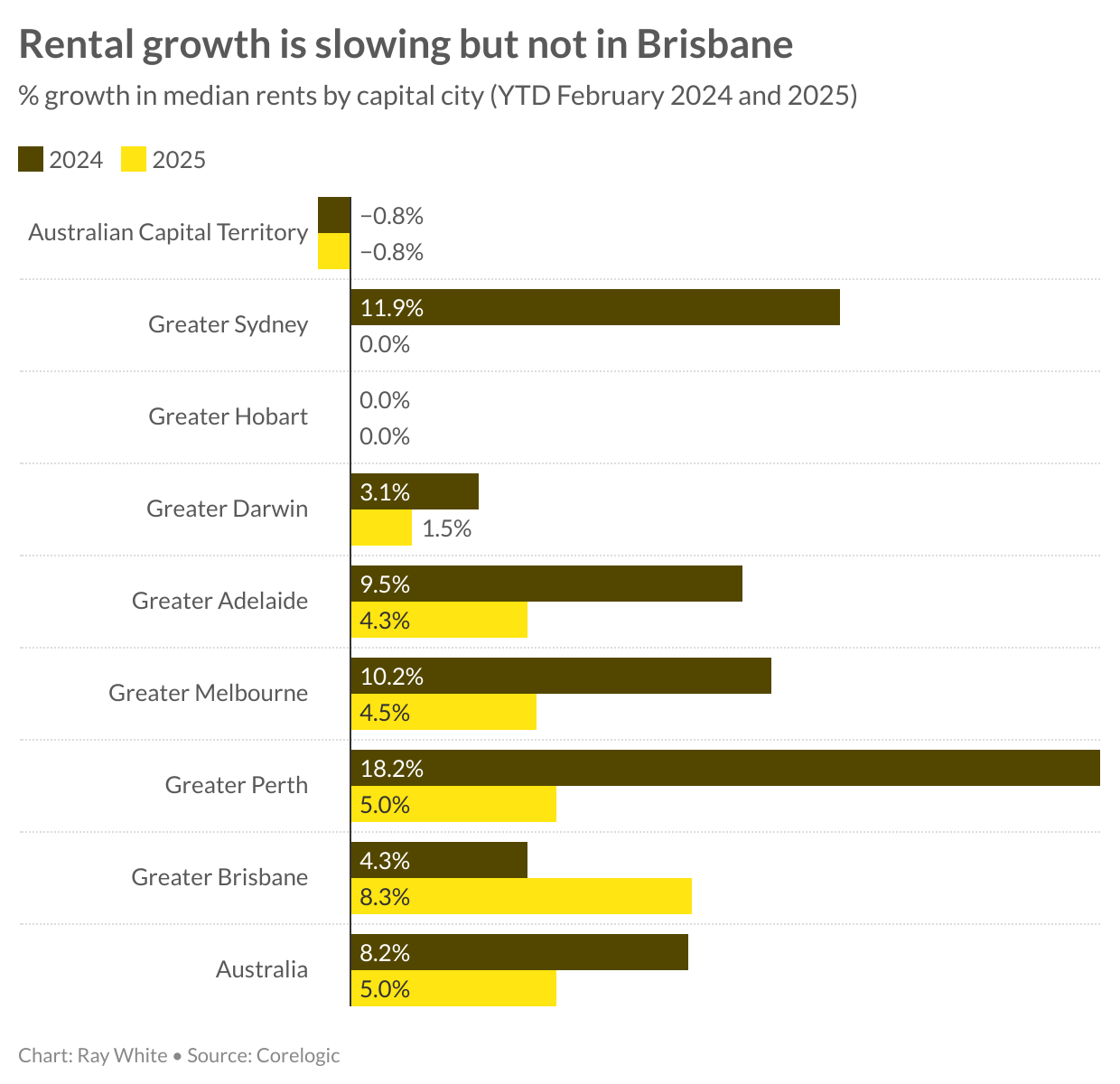

This cooling trend is consistent across most Australian capital cities—with Sydney's growth dropping from 11.9% to 0%, Melbourne falling from 10.2% to 4.5%, and Perth declining from a whopping 18.2% to 5.0%. However, Brisbane stands as the notable exception, with rental growth still accelerating from 4.3% to 8.3%.

Several factors explain Brisbane's divergent path. The city continues to experience high population growth from both interstate and international migration, creating persistent housing demand when other cities are seeing stabilisation. This demographic pressure is compounded by construction constraints that exist elsewhere but are more intense in Brisbane.

Brisbane's construction sector faces extraordinary challenges on multiple fronts. Major infrastructure projects are consuming significant building capacity that might otherwise be directed toward residential development. At the same time, a boom in commercial construction has further diverted limited resources away from housing. The result is a perfect storm of high demand meeting constrained supply.

The construction industry itself is struggling with the highest post-COVID cost increases among all Australian capital cities. Productivity issues and difficulties securing skilled tradies have further hampered building activity. Adding to these woes, Brisbane has seen an unusually high number of construction companies entering receivership, delaying completions. This combination of factors has created a unique situation where Brisbane's rental market continues to tighten while other cities find relief.

The recent impact of Tropical Cyclone Alfred is likely to worsen Brisbane's rental market in the short term. The storm damage has taken many rental properties out of commission while simultaneously placing additional burden on already-strained construction capacity.

While most Australian cities can expect some relief from the rapid rental increases of recent years, Brisbane renters will likely face continued pressure. The unique combination of population growth, construction limitations, and now natural disaster recovery suggests that Brisbane's rental growth will remain an outlier in the national trend toward moderation.

For renters in most of Australia, the data indicates welcome relief on the horizon—but those in Brisbane may need to prepare for a different reality for now.